Lithium Carbonate Prices Rebound Sharply — Strategic Response Required for Battery Buyers

Market Update: Prices Surpass 70,000 RMB/ton

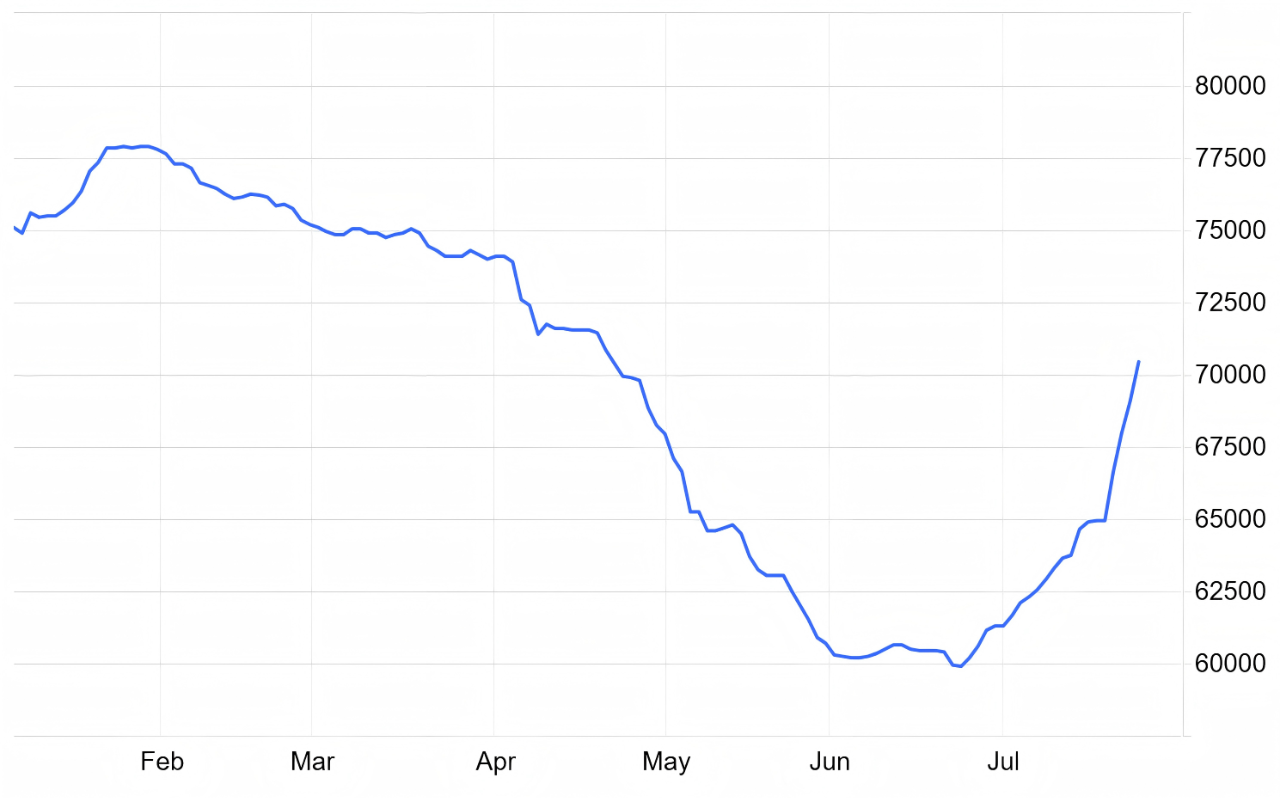

Battery-grade lithium carbonate prices in China have seen a sharp rebound since early July. As of the latest data, the spot price has reached 72,900 RMB/ton, marking a 20%+ increase month-on-month, with several consecutive days of 1,000+ RMB/ton daily gains.

This turnaround follows months of decline, where prices had dropped from over 100,000 RMB/ton in early 2024 to below 60,000 RMB/ton by June 2025. The reversal in July has been both swift and significant.

Key Drivers: Policy Signals and Market Reaction

The surge is widely attributed to strong policy signals from the Chinese government. On July 18, MIIT’s Chief Engineer Xie Shaofeng confirmed that stabilization plans for key industrial sectors—especially non-ferrous metals—are in progress. These include structural reforms, supply-side optimization, and removal of outdated capacity.

The metals market responded promptly: alongside lithium carbonate, coal, steel, and glass prices also jumped, driven by expectations of tighter supply and renewed demand momentum.

Demand Remains Strong: Energy and EV Sectors

Demand fundamentals remain robust, particularly in energy storage and electric vehicles (EVs):

NEV sales in Europe are rebounding.

China’s domestic energy storage procurement hit 46.1 GW / 186.7 GWh in H1 2025 — up 243% YoY.

Overseas energy storage orders secured by Chinese firms reached 160+ GWh, a 220% YoY increase.

The global shift toward electrification and renewable integration continues to anchor strong long-term demand for lithium batteries and raw materials.

Supply Constraints Intensify: LFP Cell Prices Set to Rise

The supply side is now showing strain:

Tier-1 cell manufacturers have begun notifying clients of imminent price increases (≥10%).

Some customers report limited or no access to high-quality LFP cells from major brands.

Tier-2 suppliers are also nearing inventory depletion.

As a result, upstream lithium carbonate costs are being passed down the chain, triggering a new wave of energy storage cell price adjustments.

Strategic Insight: Plan Ahead, Act Early

While this rebound is unlikely to return to 2022’s historic highs (600,000 RMB/ton), it marks an important inflection point. The battery industry is transitioning from high-speed expansion to value-focused, quality-driven development.

Buyers should not delay. Cell prices are already rising, and lead times are expected to lengthen. Securing supply now can minimize the financial impact.

LYTH’s Offer: Solutions Amid Volatility

At LYTH, we help clients manage uncertainty with:

Real-time insights on LFP cell pricing trends

Inventory lock-in strategies

Flexible lithium battery configurations across NEV, ESS, telecom, and commercial sectors

We also offer a strategic roadmap for sodium-ion battery integration, as the current lithium price surge gives this alternative technology a new window of opportunity.

Take Action Now

With costs rising and inventory tightening, procurement decisions must be swift and strategic. Contact LYTH today to:

✅ Lock in pre-increase pricing

✅ Discuss project-specific configurations

✅ Access secured, high-quality battery supply

📩 Reach out to our sales team now — before the next price adjustment hits.